Blog

Blog Topics

Browse the blog by topic

Choose a tag to narrow the archive, or browse the full RPSA blog below.

12 March 2026

The Single Construction Regulator

-

Andrew McColl - Chairman

Andrew McColl - Chairman

The Future of Residential Surveying: A Defining Moment for Our ProfessionA 15-minute read - So put the kettle on first.If you work in residential surveying, this moment matters to you, whether you realise it yet or not. I know...

20 January 2026

Speed, Certainty, and the Surveyor’s Role in a Transformed Market

-

Andrew McColl - Chairman

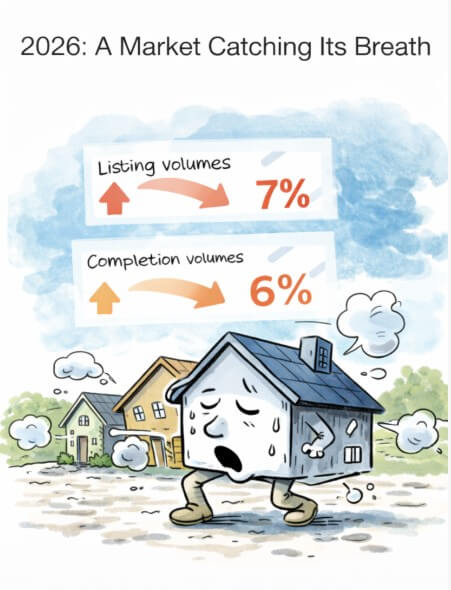

The Crossroads of 2026: Speed, Certainty, and the Surveyor’s Role in a Transformed MarketIf you had walked into any surveying event or forum in early 2024 and started talking about Artificial Intelligence, you might have been met...

24 December 2025

Damp and Mould in Survey Reports - An Essential Read

-

Kieran McColl

Kieran McColl

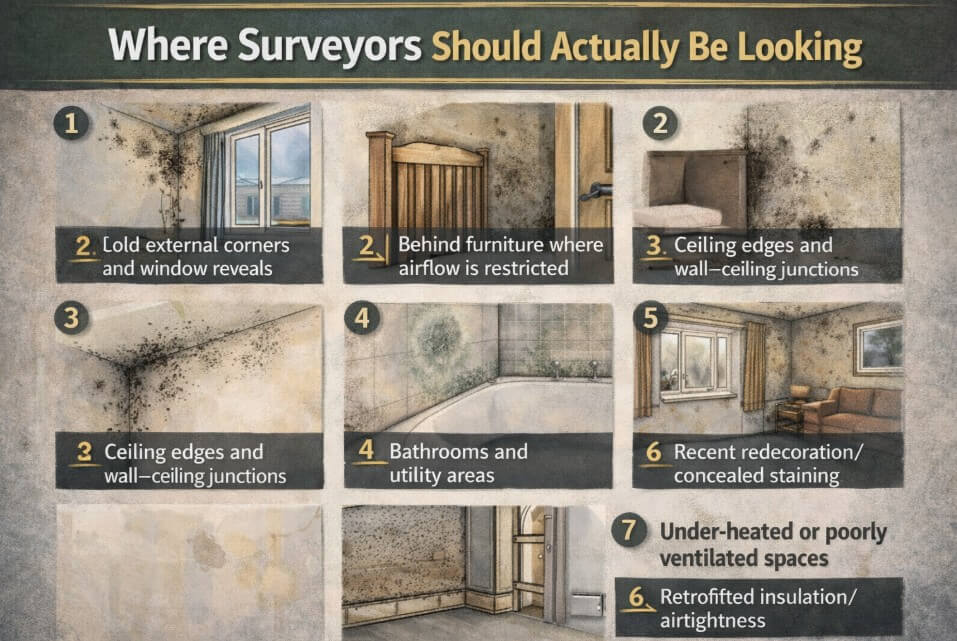

Damp and mould in survey reports: Why “mentioning it” is no longer enoughMost survey failures do not arise because a defect was missed entirely. They arise because something was seen, but not properly explained.Damp and mould are...

24 December 2025

Government Consultation - A Suggested Response

-

Andrew McColl - Chairman

Residential property surveyors association (RPSA) Response to “home buying and selling reform” consultation december 2025This is an example of how to answer the full consultation, but we appreciate that individual views may...

5 December 2025

Knotweed - Guest Blog from Emily Grant.

-

Emily Grant

Emily Grant

Invasive Plants: Data, Diagnosis and “Priceless” Member BenefitsIntroduction (by Andrew McColl):Back in March, we highlighted the rising threat of Bamboo in our newsletter ("Is Bamboo the New Knotweed?"). At the time, we...

1 December 2025

Free CPD - One for the Radar.

-

Andrew McColl - Chairman

A Goldmine of Free CPD: Why Elemental London & the NHIC Knowledge Hub Should Be on Your RadarApologies for the slight delay in sharing this write-up. It’s been a very busy few weeks across the Association, but I didn’t want this...

28 November 2025

Why Upfront Information Isn’t a Threat to Surveyors: It’s a Real Opportunity

-

Marion Ellis - RPSA member and Founder of Love Surveying

Marion Ellis - RPSA member and Founder of Love Surveying

Over the past few weeks, I’ve had more messages from surveyors than I’ve had in years. Some were reassuring (“I’m glad someone has explained this properly”), some were worried, and many said the same thing in different ways: “ I...

27 November 2025

Autumn Budget 2025 – What It Actually Means for Residential Surveyors

-

Andrew McColl - Chairman

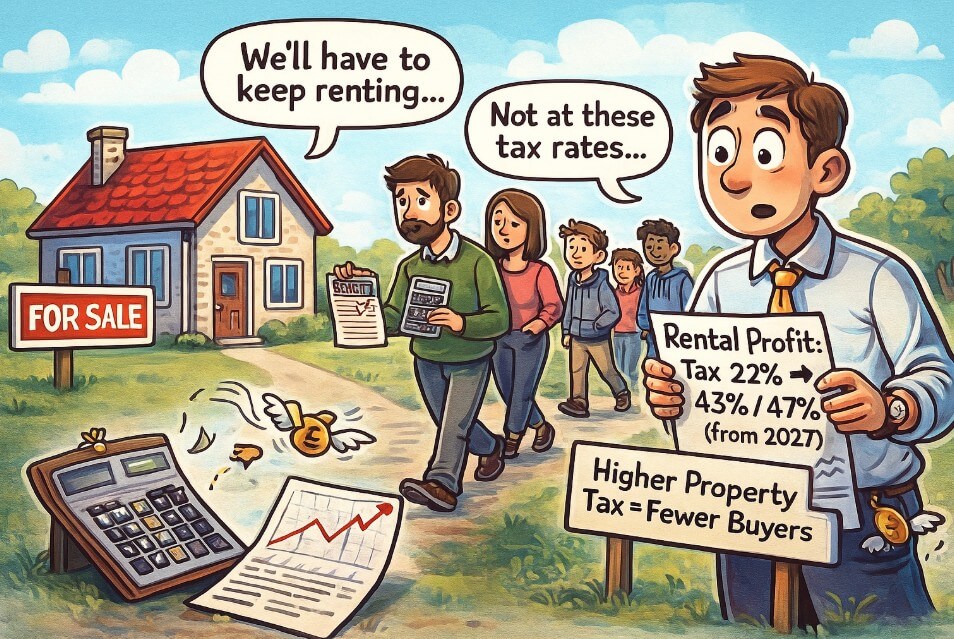

A Straightforward Analysis from a Fellow Taxpayer.Like most of you, I watched the Budget waiting for the bits that hit us hardest.Here’s the plain-English version – no spin, no 154-page jargon – just the changes that will affect...

17 November 2025

Home Buying & Selling Reform - Don't Ignore It

-

Andrew McColl - Chairman

Home buying & selling reform – why this consultation should seriously concern every independent surveyorThe Government has released its consultation on Home Buying and Selling Reform. After a thorough review of all 28...

12 September 2025

RPSA at the CABE Centenary Celebration

-

Andrew McColl - Chairman

On 12 September, I had the pleasure of joining my fellow Council member, Malcolm Hordern, at the Chartered Association of Building Engineers’ (CABE) 100th birthday celebrations at Stanbrook Abbey in Worcester.The heavens did open...

21 August 2025

New Kid on the Block - The "Insight" Survey

-

Andrew McColl - Chairman

New Survey Debut - Hats Off to Such a Game-Changing Initiative.Seller’s surveys: A fresh tool for a stalled marketAs Chairman of the RPSA, I’m always on the lookout for new initiatives that can genuinely help our profession...

30 July 2025

You’re All Going to Die (but Your Family Doesn’t Have to Suffer): Why Wills Are Essential for Surveyors—and Everyone Else

-

Andrew McColl - Chairman

I know what you’re thinking Andrew’s lost the plot, going on about Wills. Isn’t this what we ignore until retirement? Trust me, even if you’re not quite at the ‘cruises and croquet’ stage, this is the most essential admin you’ll...

8 July 2025

Franchise Spotlight: A Closer Look at Property Inspections Franchise Ltd

-

Andrew McColl - Chairman

A Practical Route into Self-Employment for SurveyorsDeclaring a potential interest and fostering community growthBefore you delve into the details of this blog post, I believe it's essential to declare a potential interest...

3 July 2025

Condensation, Mould & Teenage Vampires: A Surveyor’s Guide to Risk and Responsibility

-

Andrew McColl - Chairman

As building surveyors, we encounter issues with dampness, mould, and condensation on a daily basis. But how often do we pause to think about what's causing it, what’s changed in recent legislation, and just how much our advice...

2 July 2025

Elevating Safety: Essential Work at Height Guidance for Residential Surveyors

-

Andrew McColl - Chairman

Navigating real-world risks and legal duties during property inspectionsIntroduction: Why height safety matters in residential surveyingResidential property surveying inherently involves tasks that necessitate working at height...

1 July 2025

Unlock Your Potential: 10% Off All SAVA Training for RPSA Members

-

Andrew McColl - Chairman

Your Edge in a Dynamic IndustryReady to take your surveying career to the next level? In an industry where expertise sets you apart, the RPSA is committed to helping you stay ahead. That’s why we’re excited to offer an exclusive...

27 June 2025

It All Started With a Phone Call: Navigating Surveyor Liability in a Connected World.

-

Andrew McColl - Chairman

I. Introduction: The unseen risks of a simple conversationA seemingly innocuous phone call, a brief email exchange, or even an informal chat can, in the complex world of property surveying, inadvertently open the door to...

1 June 2025

Lights, Camera, Action: A Day at Black Cherry Studio – And Why Surveyors Should Embrace the Digital Age

-

Andrew McColl - Chairman

Let’s be honest: most surveyors didn’t get into this line of work because we dreamed of being on camera. Many of us are far more comfortable behind a damp meter than in front of a lens. Personally, I’ve always said I’ve got a...

1 June 2025

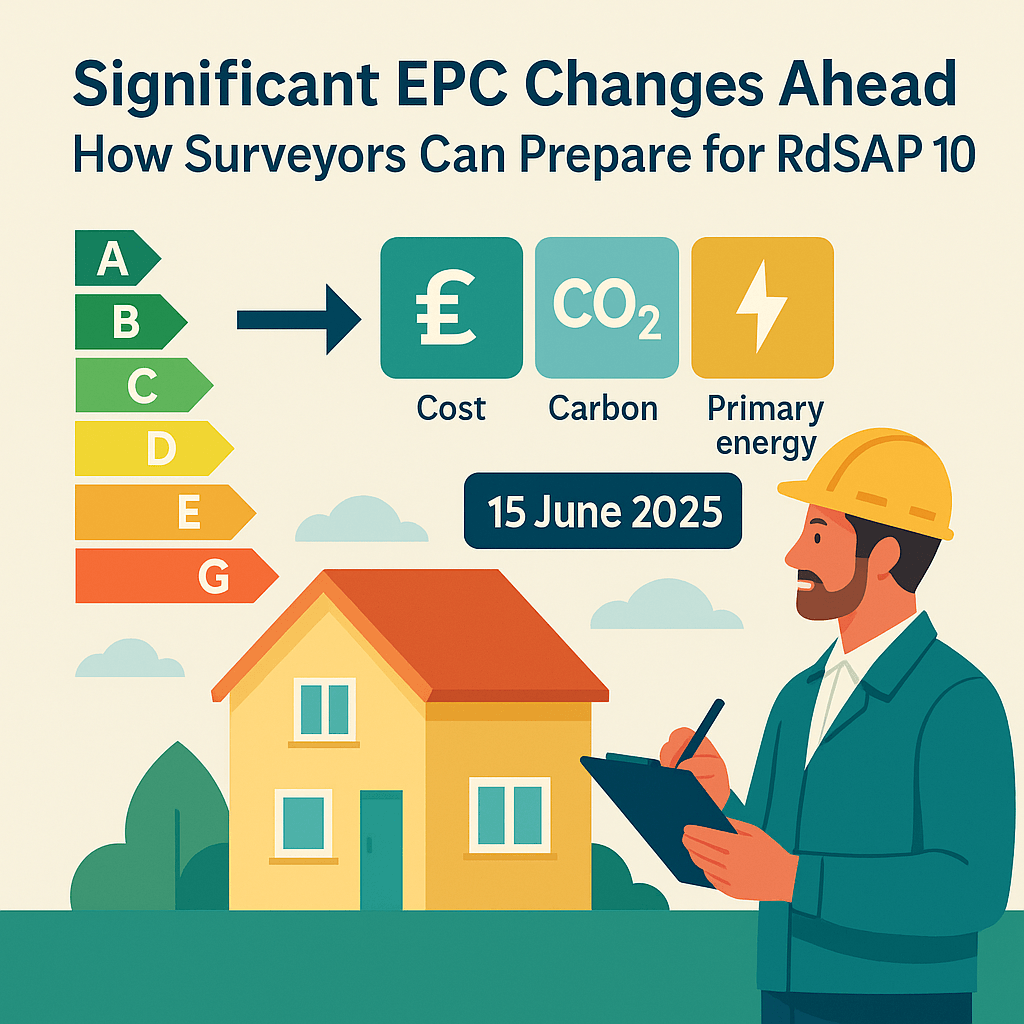

Significant EPC Changes Ahead: How Surveyors Can Prepare for RdSAP 10

-

Andrew McColl - Chairman

Just when we thought EPCs had settled down, they're changing again—but this time, the updates are substantial. As you are aware, EPCs have been part of the property landscape since 2008, but they haven't had the best reputation...

31 May 2025

RPSA Chairman Andrew McColl With PCA CEO Sarah Garry

-

Andrew McColl - Chairman

A collaborative conversation: RPSA chairman Andrew McColl with PCA CEO Sarah GarryWe recently sat down with Sarah Garry, CEO of the Property Care Association (PCA), for an insightful discussion on her journey, the PCA's strategic...

18 May 2025

A Pathway of Recognition for Residential Surveyors

-

Andrew McColl - Chairman

Hello everyone,We recently hosted a significant webinar with the Chartered Association of Building Engineers (CABE) to introduce their new Residential Surveying Section (RSS). This initiative represents a fantastic opportunity...

16 May 2025

Why No Residential Surveyor Can Afford to Ignore It

-

Andrew McColl - Chairman

By Andrew McColl, chairman, residential property surveyors association (RPSA)At a recent Property Institute event, many of us were struck by a key message from Sandra Ashcroft, Head of Industry Competence and Culture Change...

12 May 2025

What the Law Society's Note Means for RPSA Members

-

Andrew McColl - Chairman

Surveying in a Changing Climate: What the Law Society's Note Means for RPSA MembersA friendly heads-up: Why this article matters to youHello fellow RPSA members! We've put this article together because, as you know, the world...

12 August 2024

Property and Surveying Industry Update

-

Alan Milstein, Chairman

Alan Milstein, Chairman

Read all the latest surveying industry news in just 3 minutes right HERE

30 November 2023

Why Material Information Is Important for Surveyors

-

Alan Milstein, Chairman

3 Minute ReadWhy material information is important for surveyorsOn 30th November 2023, the snappily titled National Trading Standards Estate and Letting Agency Team (NTSELAT) made their long-awaiting (and delayed) announcement...

10 February 2023

Why Good PII Matters

-

Alan Milstein, Chairman

Every member of the RPSA endeavours to deliver a high quality and consistently reliable service to their client on every occasion.But, as in any walk of life, despite our utmost efforts, sometimes, something goes wrong. And that...

22 November 2022

Benefits of Being an RPSA Member

-

Alan Milstein, Chairman

Being a member of the RPSA is not just about being part of a professional association that stands for the highest standards in our industry.As a valued member of the RPSA we can offer a range of benefits to support you in your...

31 December 2021

Review of 2021 and Looking Ahead to 2022

-

Alan Milstein, Chairman

WAYTW!What a year that was! Want to find out more? Spend just 5 minutes to read about all we've done.What we have achieved at the RPSA over the last 12 months is nothing short of astounding. But it has let us set in place the...

17 December 2021

Oh! What a Day It Was! RPSA Conference 2021

-

Alan Milstein, Chairman

If you didn't make it to the 2021 RPSA Conference, "Reach for the Stars" held at the National Space Centre in Leicester, what a day you missed.The biggest, boldest and most exciting event in the history of the RPSA, delegates...

10 November 2021

Why the RPSA Launched New Snagging Standards

-

Alan Milstein, Chairman

Many RPSA surveyors have, from time to time, been asked to carry out snagging surveys on new build property. Often, though, when they have tried to book in for the inspection they have been refused access to the site by the...